Google has been bettering its algorithm to throw one-liners for search queries with wh-questions.

If you google, ‘How to Start Investing as a college student’, you should ideally get a search result at the top which says StockPe.

This blog is NOT intended for marketing!

But, this blog is not intended for marketing . In this blog, let us undertake an explorative journey and formulate a customizable plan. This plan will ideally fit the investment landscape available for college students in India.

At the end, if you land at StockPe, we get the bragging rights. ‘Bazinga! We told you so!’

Investing in Western countries or other South-East Asian countries predominantly revolves around,

- Personal Finance for International Students

- Exorbitant Tuition – Scholarships and Loans

- Tuition and Accomodation – Loan-Free Budgeting.

However, in the Desi landscape, there are barely any international students. International students in India are concentrated in very few universities and colleges. Diversity of International Diaspora is limited in these few universities as well.

The Desi ecosystem is rapidly changing. Students have the need to start investing early, to save up for further education and to hustle to explore revenue streams.

This blog is NOT How to Start Earning?

Adequate blogs have already been written on,”How to start earning when you are XX?’.

Most of these blogs, talk about

- Gigs

- Internships

- Arbitraging

- Subtitling

- Video Editing

- Prepping or Teaching courses

Most of these are time-intensive methods, where you get paid for your time.

If you are an international student, most resources preach you to take a,

- Teaching Assistantship

- Research Assistantship

- Fellowship

where you can add value.

Few resources urge you to find if there’s an opening in the campus library, where you can help out.

Few talk about,

- Competitions

- Bug Bounties

- Merit Scholarships

- Grants

- Skill Roles –

- Graphic Design

- Designing Thumbnails

- No Code

- Crypto Projects

Success in Gigs and Freelance consulting largely depends on client acquisition and retention.

But very few learning resources exist to help students and young professionals manage personal finance early in their career.

The fewer resources, which do exist fail to address the real challenges and practical solutions, for students in India.

This blog addresses How to make money from money with ZERO or little money!

Here’s a foolproof step-by-step:

1. Stick to a Bulletproof Budget

Wanna start simple?

- Jot down an Expense Journal.

- Stick to your favorite method – Strike-Through, Check Off…

- Find inspiration – Bullet Journal by Ryder Caroll

- Use digital templates – Notion

- Gamify your Budget.

Tired of scrawling in heaps of notebooks ?

Exploit digital tools which make effective budgeting easy to your fullest advantage.

The competition for the best budgeting app has existed for the past decade.

With new startups with exciting functionalities like BillR and SplitWise which aimed to overtake Venmo(the Gpay like Bill sharing app) in the USA, with elevated UX and features.

Clean Tools:

- Excel

- Google Sheets

iOS Apps:

- Wally

- Buddy

Android Apps:

- Wallet

- Money Manager

OS Agnostic App:

- YNAB

Budget App for Business POS:

- Quickbook

- Khatabook

- PineLabs

Free, Free, Free:

- Goodbudget

- Mint

2. Split your Needs and Wants:

Set aside 50% of your money in hand for pertinent needs –

- Snack

- Food

- Travel

- Upskilling Expenses

- Education Expenses.

Jot down your wants –

- A flashy new iPhone.

- A shiny two-wheeler or

- A pricy weekend shopping plan

in your budget bucketlist. Do not include these as your needs.

3. No Credit:

- Don’t buy into FinTech or Loan products.

- Don’t buy your ‘Want Bucketlist’ on Loan products.

- Zero-EMI, BNPL and Salary-On-Demand are few hidden loan products with high processing charges.

- Early Credit can affect your Credit Score adversely.

- Bad Credit History can affect procuring purposeful loans in your future.

- Dedicate a day every month to jot down your credit card and compare Penalties, MAB, Tax with the previous month.

- If you have a credit card, check if certain amount of money is consistently deducted every month. – This can be an old subscription, which you dont use anymore or a scam. Report to bank, if its a scam

- If you invest in crypto, calculate gas or transaction fee wisely.

- Conduct due diligence in calculating currency conversion fee, when you try to invest in global platforms.

4. Insure:

Firstly, Bachaa Do Bavishya, with Insurance products to cover Life and Health.

- Invest in Pure Insurance Products.

- Pure Insurance Products are more legitimate than Insurance products which pose as Investment products.

- Insurance products which pose as Investment products do not yield sufficient returns.

5. Fitbit your Subscriptions:

Fitbit keeps you healthy by tracking your steps, sleep and heart rate. Similarly, tracking your subscriptions keeps your Financial health in check.

- Check subscriptions attached to all your Google and Apple accounts in Playstore and Appstore.

- Check subscriptions in Lifestyle Apps – Are you still subscribed to the Gym from your previous locality.

- Check Streaming and Magazine subscriptions.

- Check for subscriptions to tools which you don’t use anymore – proxy tools, or other tools which are hosted on a site. – Carry out this check with all your email IDs.

6. Liquid Fund for your Bucketlist:

Invest in a Liquid Fund and save up consistently for a year or two, till you have compounded enough to fulfil your short-term financial goals.

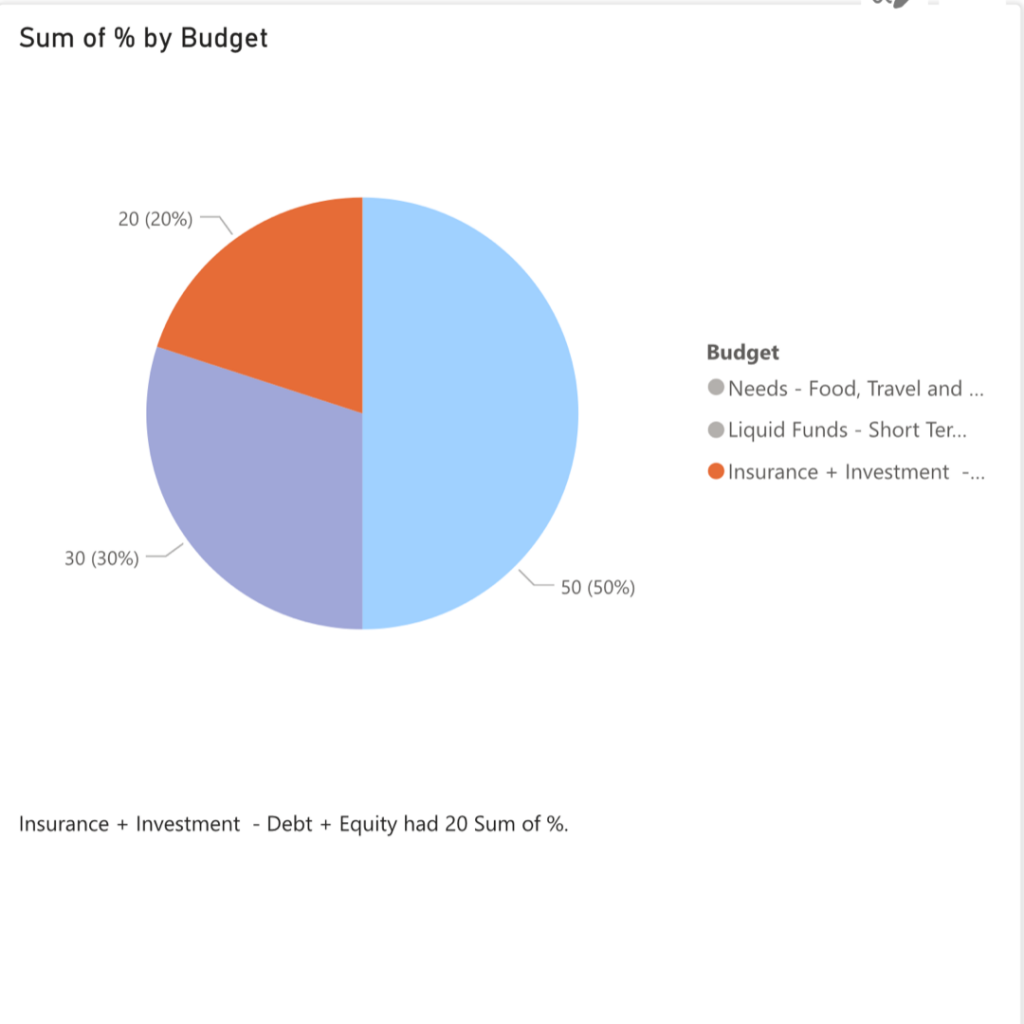

7. 50-30-20 Plan

- 50% for Needs

- 30% in a Liquid Fund

- 20% – First, Invest in a good Insurance Product

- Rest, Invest in assets, which have the potential to give healthy returns and shelter against inflation. How? Let’s Explore

8. The 20 in the 50-30-20 Plan.

This 20% is your long-term investment.

How To?

- Plan your duration during which you will consistently invest every month – 5 years, 10 years, 15 years, 20 to 30 years.

- Decide how much you want to invest every month based on your present and future plans.

- Estimate your current risk appetite.

- How much do you plan on investing when practicing how to invest.

- How much risk can you tolerate on your investments?

- Explore platforms, which offer ZERO CAPITAL and Build a Portfolio Features.

- Explore platform which lets you learn and Build Your Portfolio in Games without Losing Money.

- Choose your risk plan – 60/40, 70/30, based on how long you intend to invest. Long Risk Plans are intended for Long-Term investments,

- Decoding Risk Plans – In a 70/30 risk plan, you invest 70% in Equity – Stocks and 30% in Debt – Bonds and PPF (In the Desi context)

The ultimate platform for students to start investing with ZERO to little money in hand is – StockPe.

At StockPe tournaments, you can build your portfolio and learn finance without losing money.

")